Roughly 10,000 Americans turn 65 every day, and a significant portion of them own businesses they’d like to sell. The result is one of the largest intergenerational transfers of small business ownership in history — and a major opportunity for the right buyers. If you’re looking to acquire a business in the $500K–$5M range, the financing landscape is more accessible than it was even five years ago. CapFront has helped thousands of business owners navigate this transfer.

This guide walks through how business acquisition financing actually works in 2026: the three main paths (SBA, conventional, seller financing), how they stack and combine, what underwriting actually looks at, and the deal structures that close versus the ones that die at the lender.

The Acquisition Financing Landscape in 2026

Most small business acquisitions in this size range are financed through some combination of three sources:

- SBA 7(a) loans (the workhorse of Main Street acquisitions)

- Conventional commercial financing

- Seller financing (the seller takes back a note for part of the purchase price)

A meaningful percentage of acquisitions use all three. Understanding how they combine is often more important than understanding any one in isolation.

The Quick Decision Framework

Before we go deep, here’s the rough shorthand:

- $500K–$5M acquisition, Main Street business with real assets: SBA 7(a) is almost always the anchor.

- $5M–$15M acquisition, established business with strong cash flow: Conventional or SBA 7(a) (capped at $5M), often with seller note.

- $15M+ acquisition: Conventional commercial lending, often with mezzanine or preferred equity.

- Any size with a motivated seller: Seller financing can and should be part of the conversation.

Now let’s get into what each one actually looks like.

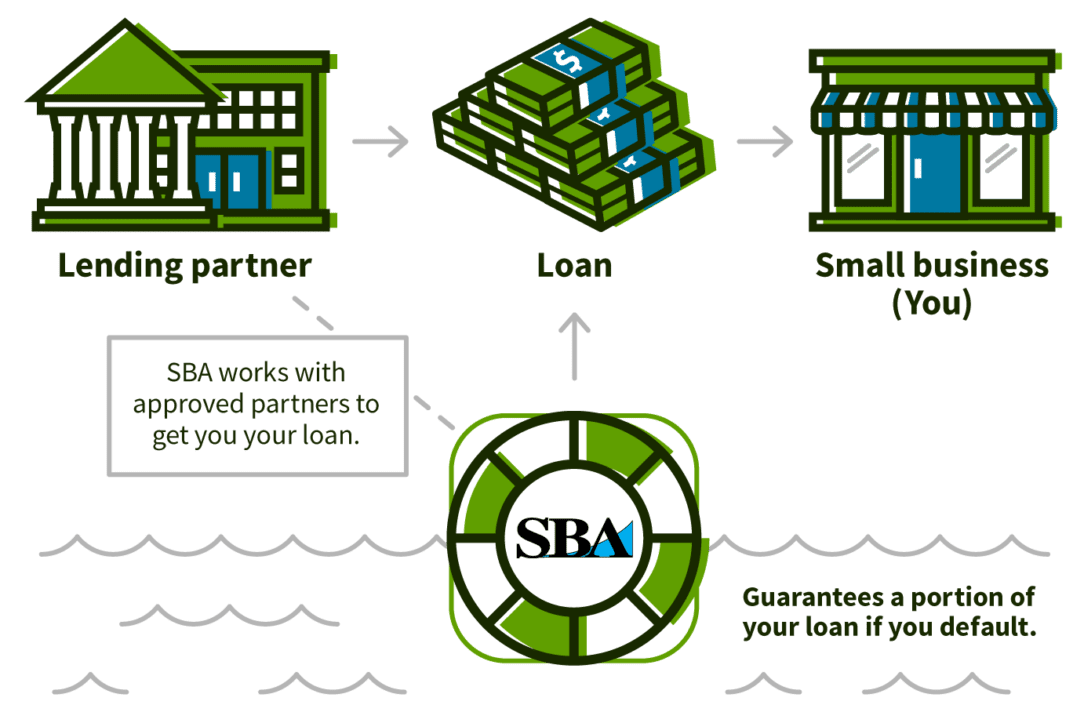

SBA 7(a) Loans for Business Acquisition

The SBA 7(a) program is the single most common financing path for small business acquisitions under $5M. For good reason — the terms are the most favorable you’ll find for a first-time business buyer.

What SBA 7(a) Acquisition Financing Looks Like

- Maximum loan size: $5 million

- Typical down payment (equity injection): 10%

- Term: Up to 10 years for non-real-estate acquisitions, up to 25 years when real estate is included

- Rate: Tied to Prime + 2.25–3.00% for most acquisition loans (so roughly 10.5–13.5% at current Prime rates)

- Personal guarantee: Required from all 20%+ owners

- Collateral: Business assets plus personal assets up to the loan amount (including home equity if available)

The 10% equity injection is often the make-or-break for first-time buyers — but it’s more flexible than you might think. The SBA allows a portion of that 10% to come from a seller note on standby (more on this below), effectively reducing your cash-out-of-pocket to as little as 5%.

How SBA Actually Underwrites an Acquisition

Unlike conventional lenders, the SBA focuses heavily on:

1. Debt Service Coverage Ratio (DSCR) on the target business. Lenders typically want the business’s historical cash flow to cover the proposed new debt service by 1.25x or more. This is calculated off the seller’s tax returns, adjusted for owner compensation, non-recurring items, and changes post-acquisition.

2. Your experience relative to the business. You don’t have to have run this exact business before, but you need a credible story for why you can run it. A buyer with 10 years of operations management acquiring a manufacturing business is a fundable story. A buyer with no related experience is a much harder file.

3. The quality of the business itself. Customer concentration (one customer over 20% of revenue is a yellow flag, over 40% is often a kill), declining revenue trends, messy books, and high seller-dependence all create issues.

4. The valuation. SBA loans require a third-party business valuation for most acquisitions. If you’ve negotiated a purchase price above what the valuation supports, you’ll either renegotiate or fund the gap with seller financing or additional equity.

Timing

An SBA 7(a) acquisition loan typically closes in 45–75 days from application to funding. Experienced SBA lenders with clean deals can sometimes close in 30–45 days.

Conventional Acquisition Financing

For acquisitions above $5M, or for buyers who want to move faster than SBA allows, conventional commercial financing is the alternative.

What Conventional Looks Like

- Typical down payment: 20–40% (significantly more than SBA)

- Term: 5–10 years, often with balloon payments

- Rate: Varies widely — 8–12% for strong borrowers with banks, higher for non-bank lenders

- Personal guarantee: Usually required, though structure varies

- Covenants: Often includes financial covenants (DSCR maintenance, capex limits, distribution restrictions)

When Conventional Beats SBA

- Deal size exceeds $5M (SBA cap)

- You need to close in under 30 days

- The business doesn’t qualify for SBA (size standards, industry exclusions, foreign ownership)

- You’d rather avoid the personal asset collateralization that SBA requires

- You have the equity to meet conventional down payment requirements

When Conventional Is Worse Than SBA

- You’re buying your first business and don’t have 25%+ down

- The business is marginal on DSCR (SBA is more flexible)

- You want a 10-year fully amortizing loan without refinance risk (conventional often has balloons)

Seller Financing

The unsung hero of small business acquisitions. In a seller-financed deal, the seller accepts part of the purchase price as a note — effectively lending you the money to buy their business.

Why Sellers Agree

- Tax advantages. Spreading sale proceeds over multiple years can meaningfully reduce total tax liability for the seller.

- Higher total price. Sellers often accept seller financing in exchange for a higher total price.

- Buyer pool. Willingness to carry paper expands the buyer pool dramatically, often producing better offers.

- Signal of confidence. A seller who’ll finance part of the deal signals to the buyer (and to the SBA lender) that they believe in the business’s continued success.

Typical Structures

- Full seller financing: Rare, usually only on smaller deals or distressed businesses. Buyer pays 10–30% down, seller carries the rest at 6–10% over 5–10 years.

- Seller note as part of stack: Common. Buyer uses SBA or conventional for 70–80%, seller note covers 10–20%, buyer injects 10% cash.

- Standby seller note: The seller note is structured so no payments are made for the first 1–2 years (or until the SBA loan is paid down to a certain point). This is what allows the note to count toward the SBA’s 10% equity requirement.

- Earnout structure: Portion of the purchase price is contingent on post-close business performance. Not technically seller financing, but often combined with one.

The Hidden Value of Seller Financing

Beyond the dollars, seller financing creates alignment. A seller carrying paper has a continuing interest in the business’s success. They’ll often stay engaged through a transition period, help with customer introductions, and share knowledge they might otherwise hold back. The value of this transitional support is genuinely hard to overstate on deals where the seller was the business.

Common Pitfalls That Kill Acquisition Deals

1. Poor seller books. If the seller’s financials are messy or if they’ve been aggressively minimizing tax liability, the cash flow won’t support the SBA underwriting. Sellers who’ve taken significant cash out of the business personally often have bigger gaps between what the business actually earns and what the tax return shows.

2. Working capital shortfalls. Many first-time buyers focus entirely on the purchase price and forget they need 2–3 months of operating working capital on day one. A $2M acquisition often needs $200–300K in additional working capital financing that has to be planned upfront.

3. Customer concentration. SBA lenders and conventional lenders both scrutinize customer concentration. Deals where one customer represents 30%+ of revenue often get restructured or declined.

4. Key employee dependence. If the business runs on one key salesperson or technical employee who may leave post-close, lenders get nervous. Retention agreements and employment contracts help.

5. Over-leveraged seller. If the seller has liens on business assets that will consume most of the sale proceeds, there may not be enough left to carry a seller note — which can undo a deal’s capital stack.

6. Price too high for cash flow. Lenders underwrite the deal’s ability to service the debt. If the purchase price requires you to pay yourself less than a market salary just to make the payments, you’re likely paying too much.

What to Prepare Before Financing Conversations

The difference between “I want to buy a business” and “I’m financeable” comes down to preparation. Before you’re having serious conversations with lenders:

- The LOI or term sheet with the seller

- 3 years of seller tax returns (business and sometimes personal)

- 3 years of P&Ls and balance sheets from the seller

- YTD financials through the most recent month

- Your personal financial statement and 3 years of personal tax returns

- Your resume with narrative on why you can run this business

- A transition plan showing what the seller’s role will be post-close

- Working capital projection for the first 12 months post-close

Having this pre-packaged cuts approval times meaningfully and signals to lenders that you’re a serious buyer.

The CapFront Approach

We finance business acquisitions in the $200K–$5M range, combining SBA, conventional, and seller-financing structures to fit the deal. Because we’ve structured a lot of these, we can often help you think through the capital stack before you’ve even locked in the purchase price.

If you’re actively looking at an acquisition, a conversation before you finalize the LOI is usually the highest-leverage hour you can spend. We’ll tell you what’s fundable, what structure to push for with the seller, and what your realistic closing timeline looks like.

Frequently Asked Questions

Can I really buy a business with 10% down? Yes, with SBA 7(a) financing. A portion of that 10% can sometimes come from a seller note on standby, meaning your actual cash out-of-pocket can be as low as 5%. This is the most common first-time buyer path.

What credit score do I need to finance a business acquisition? SBA 7(a) typically requires 680+ FICO, with 700+ preferred. Conventional lenders often want 720+. Below 680, options narrow significantly — though specialty lenders and deals with strong seller financing can still close.

Do I need industry experience to buy a business? Not necessarily, but you need a credible narrative for why you can run the specific business. Direct industry experience helps. Relevant transferable experience (operations, sales, general management) often suffices. “I’ve always wanted to own a business” is rarely enough on its own.

How long does business acquisition financing take to close? SBA 7(a): 45–75 days typical. Conventional: 30–60 days. All-seller-financed deals: 2–4 weeks. Plan for the longer end of these ranges in your purchase agreement timeline.

Can I finance a business acquisition with no money down? Very rare, but occasionally possible. 100% seller-financed deals sometimes happen on smaller transactions (under $500K) with motivated sellers. For most deals, plan on 5–10% cash minimum even with aggressive structuring.

Should I buy the business as an asset purchase or stock purchase? Most SMB acquisitions are structured as asset purchases because they isolate the buyer from the seller’s historical liabilities and often provide better tax treatment for the buyer. Stock purchases happen in specific situations (transferable licenses, contracts that can’t be assigned, certain tax situations). Talk to your CPA and attorney — this decision has significant financial consequences.

What’s the difference between an SBA 7(a) and an SBA 504 for acquisitions? SBA 7(a) can be used for business acquisition directly. SBA 504 is typically for real estate and major equipment only — it can’t finance goodwill or the business itself. Most business acquisitions use 7(a); if the deal includes significant real estate, it may combine 504 (for the real estate) and 7(a) (for the business).